AI is not just simply adding capability to existing software products. It is reshaping the software cost structure, product architecture, distribution dynamics, and margin allocation across the industry. Over the next three to five years, this shift will alter where power resides in the software stack and which companies capture durable economics.

To understand the impact, it is important to begin with today’s competitive structure.

Today’s Software Competitive Structure

The modern software ecosystem operates in layered form, and each layer captures margin differently.

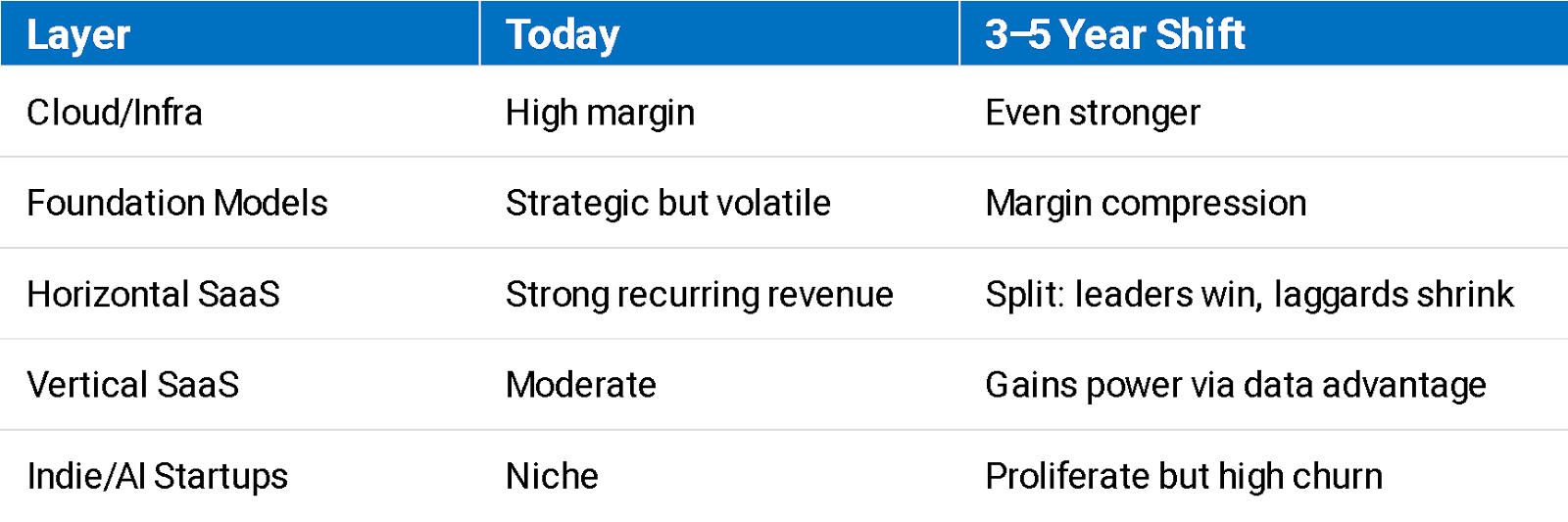

At the foundation sit the infrastructure and cloud platforms such as Amazon Web Services, Microsoft Azure, Google Cloud, and NVIDIA. They provide compute, storage, networking, AI training infrastructure, developer tooling, and platform ecosystems. At scale, they capture the highest gross margins through infrastructure rent, ecosystem lock-in economics, and increasing AI training and inference revenue. Their structural advantages are capital intensity, hardware supply chains, and large enterprise installed bases.

Above them sits the foundation model and AI platform layer, including companies such as OpenAI, Anthropic, Google, xAI, and Cohere. These firms train frontier models, provide APIs, and sell enterprise AI services. They benefit from strategic platform positioning and model access fees, but they operate under structural constraints. Massive compute costs and rapid commoditization pressure from open-source alternatives limit the durability of pure model-layer margins.

The application layer consists of vertical and horizontal SaaS platforms such as Salesforce, Adobe, HubSpot, SAP, Oracle, Workday and ServiceNow. These companies deliver workflow automation across CRM, ERP, HR, marketing, and industry-specific tools. They monetize subscription revenue supported by workflow lock-in and a data gravity advantage. Their structural strengths include installed bases, integration webs, and customer data ownership. Historically, owning the workflow has meant owning the majority of application-layer value.

Alongside these incumbents are startups and emerging SaaS players. They focus on niche workflows, new user interface paradigms, and feature-level disruption. Their advantages are speed and category redefinition. Their constraints are distribution, capital, and switching friction.

This layered equilibrium has been relatively stable. AI changes that.

The Collapse of Software Creation Costs

One of the most immediate effects of AI is the reduction in software creation cost. AI coding copilots reduce engineering headcount needs, compress time to minimum viable product, accelerate feature build cycles, and lower quality assurance effort.

We believe the result will not be fewer companies, but more. Startup formation velocity increases as the supply of innovation expands. Teams become smaller and iteration cycles faster. Competitive cloning accelerates and defensive functional moats shorten. As software creation costs go down, there will be many more people involved in developing much more software. Before it was too costly to develop the necessary software required for many new products and projects.

AI functions as a margin equalizer. Where engineering scale once drove advantage, small teams can now build competitive products. This dynamic compresses mid-tier SaaS valuations and weakens feature-only differentiation.

The Shift to AI-Native Software

AI also alters product architecture. Traditional SaaS follows a predictable flow: user to interface, interface to workflow, workflow to database. Value is embedded in structured user interfaces, processes and dashboards.

AI-native software reorganizes that flow. Interaction begins with natural language. Agents interpret intent and execute across multiple systems. The product becomes outcome-driven rather than interface-driven.

This shift moves value away from CRUD interfaces and static dashboards toward autonomous execution and embedded intelligence. The intelligence layer, not the surface UI, becomes the strategic control point.

Historically, value accrued to those who owned the workflow. In the AI era, value accrues to those who control data, compute, distribution, and autonomous execution capability. The competitive question shifts from “Who owns the UI?” to “Who owns the intelligence layer?”

Margin Migration and Compute Gravity

AI introduces compute gravity, and margins will migrate up and down the stack accordingly.

Upstream, demand for GPUs and inference capacity strengthens cloud pricing power. Infrastructure providers are positioned to capture durable rent as AI workloads scale.

In the mid-layer, margins face pressure. Open-source models improve rapidly, and cloud integration reduces the defensibility of standalone model providers.

At the application layer, outcomes depend on execution. Companies that embed AI deeply into workflows and leverage proprietary vertical data can regain power. Ownership of workflow data remains strategically significant. Those that treat AI as an incremental feature risk erosion from AI-native competitors.

Innovation Dynamics: Fragmentation and Consolidation

AI will accelerate innovation cycles. Feature parity will arrive faster. Cross-category entry will become more common. Defensive moats based purely on functionality will shorten.

At the same time, AI enables micro-SaaS companies, solo founders, and narrow tools targeting specific workflows. There will be fragmentation at the edge as creation costs fall.

However, fragmentation will coexist with consolidation. The large platforms of record, engagement and insight will remain mission critical and bundle AI capabilities across their ecosystems, integrating AI assistants, generative automation, and autonomous remediation into core products. Standalone point solutions will struggle to compete against bundled offerings.

Software categories will also converge. For example, CRM and marketing, support and sales, and adjacent functions will increasingly operate as unified AI-driven revenue systems. Platform ecosystems will likely expand as boundaries blur.

Business Model Realignment

Seat-based pricing models will weaken if AI agents replace human workflows. As automation increases and fewer human operators are required, pricing will shift toward usage-based, outcome-based, and compute-linked structures such as AI tokens.

This transition will not be uniform, but the direction is clear. AI alters not just product capability but monetization logic.

The Three-to-Five-Year Outlook

The macro outcome is margin bifurcation rather than uniform disruption.

Infrastructure providers are likely to capture durable economics driven by compute intensity. Vertical SaaS platforms with proprietary data and strong workflow ownership can remain defensible if they integrate AI deeply. AI-native incumbents will strengthen.

Mid-tier, undifferentiated SaaS platforms that rely on seat-based pricing and incremental feature expansion will be squeezed. Startup formation will increase, churn rates will rise, and M&A activity will accelerate as consolidation follows fragmentation.

AI does not dismantle the software stack. It redistributes power within it. Over the next three to five years, the companies that understand where margins are migrating, and position themselves around data ownership, compute access, distribution, and autonomous execution capability, will define the next phase of the industry.

The companies that win in this cycle will be those that rethink architecture, pricing, and workflow ownership from first principles.

If you are evaluating how AI reshapes your product architecture, pricing model, or competitive moat, book a call with us to discuss where margin is likely to migrate in your segment.